Ok so... I started getting really interested in what is my REAL expense every month.

Like I talk about being frugal and not wanting stuff in general. And I look at it from a big picture point of view, and I don't keep a budget.

So I thought... maybe there's some leakage. Maybe I've really been spending more than I think I've been spending. Maybe I think I'm frugal but actually I'm not.

Only one way to find out right?

So I took out all our bank statements and credit card bills and worked backwards. Pretty tedious... And I probably missed out some stuff here and there. Cos sometimes, my wife goes out with her colleagues or I go out with my friends and we pay first and our friends pay us back. For those I remembered, I've prorated the spending. If I forgot, then it's a data error, but doubt it would make much difference.

I've done it up as best as I could, and it's probably as far as I'm willing to go. I probably could track my own spending daily, but my wife would definitely not be cooperative to track all her expenses diligently. So, below is as best an expense update that I'm going to be able to provide.

Like I talk about being frugal and not wanting stuff in general. And I look at it from a big picture point of view, and I don't keep a budget.

So I thought... maybe there's some leakage. Maybe I've really been spending more than I think I've been spending. Maybe I think I'm frugal but actually I'm not.

Only one way to find out right?

So I took out all our bank statements and credit card bills and worked backwards. Pretty tedious... And I probably missed out some stuff here and there. Cos sometimes, my wife goes out with her colleagues or I go out with my friends and we pay first and our friends pay us back. For those I remembered, I've prorated the spending. If I forgot, then it's a data error, but doubt it would make much difference.

I've done it up as best as I could, and it's probably as far as I'm willing to go. I probably could track my own spending daily, but my wife would definitely not be cooperative to track all her expenses diligently. So, below is as best an expense update that I'm going to be able to provide.

Even so, I have some estimates.

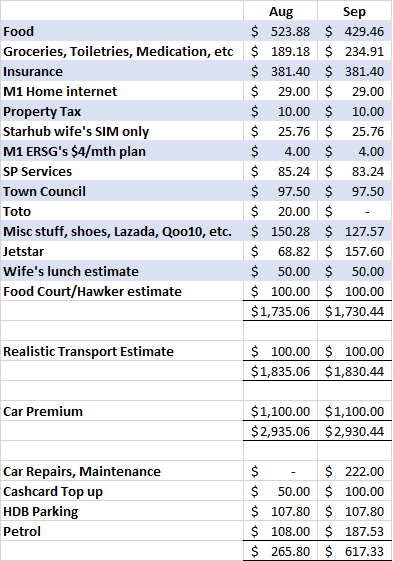

Wife's lunch estimate is at $50. This is a reasonable estimate. Her office has a canteen which serves subsidized meals.

Food Court/Hawker estimate is at $100. Likely this is over-estimated. We only go to food courts on Fri/Sat/Sun, although more often than not, we would be eating at a restaurant, so it's likely found in the Food section. At most we go to food court once a week. So $100 is likely an over-estimate.

Cash transactions are pretty hard for us to track, cos we withdraw a lump sum and keep it in the drawer and we just take from that whenever the money in our wallets run low. But we hardly spend cash cos most of our transactions are by credit card anyway. Usually this money is used for food courts.

The car expense is a bit troublesome. Cos we don't pay this on a monthly basis. The car is fully paid up and maintenance costs are lumpy on certain months. I've listed the real outflow for those 2 months, but a better estimate for car expense is $1,200 per month, with everything included. This includes the depreciation, maintenance, tax, insurance, parking, ERP, etc.

So I've put this as an estimate, $100 for reasonable transport costs if my wife worked in the CBD area, where she used to work. And I've added the car premium of $1,100. Cos if my wife leaves this job, the car premium expense will go away and she goes back to taking MRT.

Currently, she gets the option of taking a car allowance or taking the company bus. Obviously, we took the car allowance.

Jetstar expense is when I follow my wife on biz trips. So sometimes it appears as an expense item, sometimes it doesn't.

I've intentionally included a Toto expense in there. Cos some months we buy, some months we don't. I'm not going to quibble over an additional $20. If I wanted to cut costs, I would start at the Food and Grocery section.

We went to Taiwan for holiday in August. So the August expense includes the meals in Taiwan. But the flight and accommodation were prepaid so, I suppose August is a good month to include in my estimations. Cos it contains a proportion of travel expense.

Our mortgage payments are also not included. Cos I think it's hard to really quantify this as an expense.

Some people take a 20 year loan, others take a 30 year loan. Some people buy a bigger place, other's buy a smaller place. If we wanted to calculate expense, then we would need to separate out the interest and home equity payments. Cos the home equity should be considered an investment. So, I'd prefer not to compare this portion. I stay in a 4 room HDB. You can do your own estimations.

My wife's CPF and income tax are not included. Also excluded are the amounts we give to our parents. Both we'd prefer to keep private.

Now that I've listed out my own expense. I'm quite pleased actually. Cos I think we're doing pretty well without a budget. Not much leakage in my opinion.

Where do I think I could do better?

Well... the car is a glaring issue. The alternative is for my wife to take Uber/Taxi, both of which are likely to incur similar expenses as car ownership considering area where she works and the time she needs to get to office. Else she takes the company bus, but that's not wise, cos she she gets a car allowance, and this can be used to negotiate a higher fixed pay if she ever changes her job.

Our insurance expense is pretty high. But I'm not going to drop that. We have some Critical Illness covers and Early Critical Illness covers, so those are the more expensive products. All my insurance are term products.

The Jetstar and Toto expenses are probably easy to drop. I could just choose not to follow my wife on her trips. Or I could just choose not to buy Toto.

Alternatively, we could just not indulge in our sashimi habit. I think that's likely a $100 per month luxury. Or we could eat at cheaper restaurants. So instead of $50 per couple, we could just eat something else at $30 per couple...

I reckon it would be really easy to shave off $200 per month without much issue. And we'd likely not even feel it in our lives. Straight off $100 savings from sashimi, and I don't follow her on her business trips. There... that would have saved us over $400 over the past 2 months.

But I don't think that's how life should be. I think we should all allow ourselves some spending to make life a little more fun. Else what's the point in living right... Rather, to not over indulge ourselves and spend on the few things that we really enjoy doing. Cannot be indulge in everything. Then that's just over-indulgence and hardly frugal. I think, if we can afford it, to just pick a few things that really mean a lot to us and enjoy it well.

Interestingly, my estimate from my previous post isn't too far off. I had estimated it to be S$3,115.

I think this is due to us limiting our spending to our 2 UOB cards. Cos once the $500 per person is hit, we drop the spending to a very minimum level.

If I look at it another way, the UOB spending is "fixed" at S$1,000. I just get to play around with what to spend on.

The other stuff, like town council, utilities, car, telco, insurance are also considered pretty much "fixed".

So essentially... my monthly spending is pretty much all "fixed" costs. Cos the 2 UOB cards provide the limit where I should stop my spending.

I'm not going to do this next month to track my expenses. I do not take any pleasure in tracking my expenses. Cos I think it's just plain unnecessary. Cos I have no real desire to want things, so I have no real desire to spend. Some months, I'm even inducing spending just so I can push our spending up to hit the S$1,000 for our UOB cards.

I tend to live around estimates and I find that good enough for my tracking and expense management purposes.

I didn't do this exercise to find out where I can cut my spending. I was just interested if my real spending was what I expected. At least now, I know that I'm not deluded. My estimations are fair enough and I'll likely continue this level of spending.

As for the car... well, that pretty much depends on what my wife does.

<<PREVIOUS POST // NEXT POST>>

Did you like this post? If so, could you "blanjah" me 1/4 cup of my morning coffee pls.

Many thanks for continuing to come to this blog to read my posts.

Wife's lunch estimate is at $50. This is a reasonable estimate. Her office has a canteen which serves subsidized meals.

Food Court/Hawker estimate is at $100. Likely this is over-estimated. We only go to food courts on Fri/Sat/Sun, although more often than not, we would be eating at a restaurant, so it's likely found in the Food section. At most we go to food court once a week. So $100 is likely an over-estimate.

Cash transactions are pretty hard for us to track, cos we withdraw a lump sum and keep it in the drawer and we just take from that whenever the money in our wallets run low. But we hardly spend cash cos most of our transactions are by credit card anyway. Usually this money is used for food courts.

The car expense is a bit troublesome. Cos we don't pay this on a monthly basis. The car is fully paid up and maintenance costs are lumpy on certain months. I've listed the real outflow for those 2 months, but a better estimate for car expense is $1,200 per month, with everything included. This includes the depreciation, maintenance, tax, insurance, parking, ERP, etc.

So I've put this as an estimate, $100 for reasonable transport costs if my wife worked in the CBD area, where she used to work. And I've added the car premium of $1,100. Cos if my wife leaves this job, the car premium expense will go away and she goes back to taking MRT.

Currently, she gets the option of taking a car allowance or taking the company bus. Obviously, we took the car allowance.

Jetstar expense is when I follow my wife on biz trips. So sometimes it appears as an expense item, sometimes it doesn't.

I've intentionally included a Toto expense in there. Cos some months we buy, some months we don't. I'm not going to quibble over an additional $20. If I wanted to cut costs, I would start at the Food and Grocery section.

We went to Taiwan for holiday in August. So the August expense includes the meals in Taiwan. But the flight and accommodation were prepaid so, I suppose August is a good month to include in my estimations. Cos it contains a proportion of travel expense.

Our mortgage payments are also not included. Cos I think it's hard to really quantify this as an expense.

Some people take a 20 year loan, others take a 30 year loan. Some people buy a bigger place, other's buy a smaller place. If we wanted to calculate expense, then we would need to separate out the interest and home equity payments. Cos the home equity should be considered an investment. So, I'd prefer not to compare this portion. I stay in a 4 room HDB. You can do your own estimations.

My wife's CPF and income tax are not included. Also excluded are the amounts we give to our parents. Both we'd prefer to keep private.

Now that I've listed out my own expense. I'm quite pleased actually. Cos I think we're doing pretty well without a budget. Not much leakage in my opinion.

Where do I think I could do better?

Well... the car is a glaring issue. The alternative is for my wife to take Uber/Taxi, both of which are likely to incur similar expenses as car ownership considering area where she works and the time she needs to get to office. Else she takes the company bus, but that's not wise, cos she she gets a car allowance, and this can be used to negotiate a higher fixed pay if she ever changes her job.

Our insurance expense is pretty high. But I'm not going to drop that. We have some Critical Illness covers and Early Critical Illness covers, so those are the more expensive products. All my insurance are term products.

The Jetstar and Toto expenses are probably easy to drop. I could just choose not to follow my wife on her trips. Or I could just choose not to buy Toto.

Alternatively, we could just not indulge in our sashimi habit. I think that's likely a $100 per month luxury. Or we could eat at cheaper restaurants. So instead of $50 per couple, we could just eat something else at $30 per couple...

I reckon it would be really easy to shave off $200 per month without much issue. And we'd likely not even feel it in our lives. Straight off $100 savings from sashimi, and I don't follow her on her business trips. There... that would have saved us over $400 over the past 2 months.

But I don't think that's how life should be. I think we should all allow ourselves some spending to make life a little more fun. Else what's the point in living right... Rather, to not over indulge ourselves and spend on the few things that we really enjoy doing. Cannot be indulge in everything. Then that's just over-indulgence and hardly frugal. I think, if we can afford it, to just pick a few things that really mean a lot to us and enjoy it well.

Interestingly, my estimate from my previous post isn't too far off. I had estimated it to be S$3,115.

I think this is due to us limiting our spending to our 2 UOB cards. Cos once the $500 per person is hit, we drop the spending to a very minimum level.

If I look at it another way, the UOB spending is "fixed" at S$1,000. I just get to play around with what to spend on.

The other stuff, like town council, utilities, car, telco, insurance are also considered pretty much "fixed".

So essentially... my monthly spending is pretty much all "fixed" costs. Cos the 2 UOB cards provide the limit where I should stop my spending.

I'm not going to do this next month to track my expenses. I do not take any pleasure in tracking my expenses. Cos I think it's just plain unnecessary. Cos I have no real desire to want things, so I have no real desire to spend. Some months, I'm even inducing spending just so I can push our spending up to hit the S$1,000 for our UOB cards.

I tend to live around estimates and I find that good enough for my tracking and expense management purposes.

I didn't do this exercise to find out where I can cut my spending. I was just interested if my real spending was what I expected. At least now, I know that I'm not deluded. My estimations are fair enough and I'll likely continue this level of spending.

As for the car... well, that pretty much depends on what my wife does.

<<PREVIOUS POST // NEXT POST>>

Did you like this post? If so, could you "blanjah" me 1/4 cup of my morning coffee pls.

Many thanks for continuing to come to this blog to read my posts.

RSS Feed

RSS Feed