I think many people have noticed or may be interested in my/our portfolio.

But I don't write about it.

Why? You may ask... it's supposed to be interesting right?

I should write about it to share right?

You see... to me, my portfolio is not important...

Why? Sounds ridiculous? How can by portfolio be not important?!?!

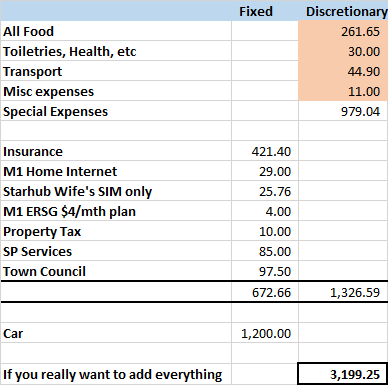

You see... Using my expense in March...

But I don't write about it.

Why? You may ask... it's supposed to be interesting right?

I should write about it to share right?

You see... to me, my portfolio is not important...

Why? Sounds ridiculous? How can by portfolio be not important?!?!

You see... Using my expense in March...

Let's look at just me.

Cos putting my wife's numbers in just clouds the numbers cos of her work.

Fixed expenses are $680 (rounded up) divide by 2 = $340

(can't be bothered to adjust for the difference in handphone bill)

Car is removed.

Discretionary expense is just the red portion divided by 2.

$350 (rounded up) divide by 2 = $175

So my personal living expenses is around $515 per month.

I haven't counted my holidays and all that, maybe I need dental treatment, etc...

So let's just say I double this amount as a "sinking fund" to balance out the whole years worth of expense.

So my living expenses is $515 x 12 = $6,120 per annum

And my holiday/other misc sudden expenses is $6,120 per annum.

(Usually my holidays are $1,500 for 2 pax so total holiday expense for 1 pax in a year is around $3k, this leaves $3k for other misc expenses.

Read about my holiday frequency and how I view it here.

Ok so let's use $12,000 total, it's easier to calculate.

How should I sustain $12,000 in annual expenses?

1) $100,000 x 12% = $12,000

2) $250,000 x 4.8% = $12,000

3) $500,000 x 2.4% = $12,000

4) $1,000,000 x 1.2% = $12,000

So if I said I have $500,000 and make 5% on it, how does that help readers?

Or if I said I have $1,000,000 and make 2% on it? What difference does it make?

Any AUM that can sustain my $12,000 a year expense will suffice.

(Although I think $12k is really overstating it...)

Everyone has their own feelings of what return they feel they obtain.

Some people think they can get 10% per annum, others like 2% per annum in stable assets.

Each one has his own sense of security and buffer required.

Some people want $2,000,000 and 5% return and must be able to cover double the expense before they are willing to leave their job.

Read about frugality for the sake of frugality here.

For me, I feel I have a minimum state of survival. I need less than $12,000 per year and I feel I live a very rich life already.

And for me, I would like to share this part, the idea that you can also live a very rich life without much money.

No matter how much assets I have or don't have.

If someone has $2,000,000 and still feels insecure about living a good life, knowing what assets I have won't give him any more security.

I also don't want people to think... Oh ERSG has $XXX worth of assets that's why he feels secure to leave his job. Or OH he has so little assets, I can't imagine he dares to leave his job with so little assets.

This just distracts from what I would like to share.

People tend to just look at the AUM and think... Oh if only I had... etc etc.

To me, insecurity and AUM are very different things.

Amount spent and a rich life are also very different.

One can have a lot of money but still feel insecure, EVEN IF, he spends very little.

One can have little money but feel secure, BUT, he must also spend very little. (I'm closer to this example.)

One can have a rich life regardless of level of spending. It is what he/she fills his life with. Friends, family, worthy activities, being true to yourself, etc.

If I told you I had $100,000, many would say that's not enough.

If I said I have $200,000 some would say I have enough, many still won't think it's enough.

If I said I have $500,000, more would said it is enough, but still many would think it's not enough.

If I said I have $1,000,000, many would say it's enough, but STILL a number would think it's insufficient.

You see. Each of us already has our own magic number...

BUT, after hitting that magic number. Are you willing to pull the trigger?

Or are you going to just make the magic number bigger just to delay things?

This is what I would like to share.

Read about the fear here.

Or are you procrastinating cos you are comfortable?

That's fine as well. Being comfortable is cool as well.

It's just being aware of it and making a conscious decision instead of feeling unhappy about work and wondering what it's like to just leave without a job.

Read about living a life without regret here.

So you see... that's why I don't share my portfolio or talk about it.

Cos it doesn't mean anything. Everything is within yourself.

How happy you are with life, your securities, your insecurities, how much you feel you need, whether you are procrastinating, what you fill your life with...

It's all about you.

And even more so... I've come to realize that the portfolio is hardly the most important thing to make someone happy. Or leaving your job.

Read about happiness is a decision here.

Some people are happy working, some people are happy working part time and get sufficient money but not a lot of money. Others are comfortable and just hang around in the job and just feeling contented but not necessarily happy.

And all of these are all ok.

So I tend to like to share all these other factors of life instead of talk about the portfolio.

And leave the portfolio and investments to other bloggers, or in the readers own hands.

*Hmm... or maybe my portfolio is too small and I don't want to share it or discuss it. Hahaha...

** This post is supposed to be posted on Monday cos I'm travelling and probably won't have time to write much. Unfortunately, I clicked post and Weebly doesn't allow me to unpost, so... Maybe Monday won't have a post, depends if I have time to write one.

<<PREVIOUS POST // NEXT POST>>

Did you like this post? If so, could you "blanjah" me 1/4 cup of my morning coffee pls.

You may also consider subscribing to receive the articles in your email, link in the column on the right.

Cos putting my wife's numbers in just clouds the numbers cos of her work.

Fixed expenses are $680 (rounded up) divide by 2 = $340

(can't be bothered to adjust for the difference in handphone bill)

Car is removed.

Discretionary expense is just the red portion divided by 2.

$350 (rounded up) divide by 2 = $175

So my personal living expenses is around $515 per month.

I haven't counted my holidays and all that, maybe I need dental treatment, etc...

So let's just say I double this amount as a "sinking fund" to balance out the whole years worth of expense.

So my living expenses is $515 x 12 = $6,120 per annum

And my holiday/other misc sudden expenses is $6,120 per annum.

(Usually my holidays are $1,500 for 2 pax so total holiday expense for 1 pax in a year is around $3k, this leaves $3k for other misc expenses.

Read about my holiday frequency and how I view it here.

Ok so let's use $12,000 total, it's easier to calculate.

How should I sustain $12,000 in annual expenses?

1) $100,000 x 12% = $12,000

2) $250,000 x 4.8% = $12,000

3) $500,000 x 2.4% = $12,000

4) $1,000,000 x 1.2% = $12,000

So if I said I have $500,000 and make 5% on it, how does that help readers?

Or if I said I have $1,000,000 and make 2% on it? What difference does it make?

Any AUM that can sustain my $12,000 a year expense will suffice.

(Although I think $12k is really overstating it...)

Everyone has their own feelings of what return they feel they obtain.

Some people think they can get 10% per annum, others like 2% per annum in stable assets.

Each one has his own sense of security and buffer required.

Some people want $2,000,000 and 5% return and must be able to cover double the expense before they are willing to leave their job.

Read about frugality for the sake of frugality here.

For me, I feel I have a minimum state of survival. I need less than $12,000 per year and I feel I live a very rich life already.

And for me, I would like to share this part, the idea that you can also live a very rich life without much money.

No matter how much assets I have or don't have.

If someone has $2,000,000 and still feels insecure about living a good life, knowing what assets I have won't give him any more security.

I also don't want people to think... Oh ERSG has $XXX worth of assets that's why he feels secure to leave his job. Or OH he has so little assets, I can't imagine he dares to leave his job with so little assets.

This just distracts from what I would like to share.

People tend to just look at the AUM and think... Oh if only I had... etc etc.

To me, insecurity and AUM are very different things.

Amount spent and a rich life are also very different.

One can have a lot of money but still feel insecure, EVEN IF, he spends very little.

One can have little money but feel secure, BUT, he must also spend very little. (I'm closer to this example.)

One can have a rich life regardless of level of spending. It is what he/she fills his life with. Friends, family, worthy activities, being true to yourself, etc.

If I told you I had $100,000, many would say that's not enough.

If I said I have $200,000 some would say I have enough, many still won't think it's enough.

If I said I have $500,000, more would said it is enough, but still many would think it's not enough.

If I said I have $1,000,000, many would say it's enough, but STILL a number would think it's insufficient.

You see. Each of us already has our own magic number...

BUT, after hitting that magic number. Are you willing to pull the trigger?

Or are you going to just make the magic number bigger just to delay things?

This is what I would like to share.

Read about the fear here.

Or are you procrastinating cos you are comfortable?

That's fine as well. Being comfortable is cool as well.

It's just being aware of it and making a conscious decision instead of feeling unhappy about work and wondering what it's like to just leave without a job.

Read about living a life without regret here.

So you see... that's why I don't share my portfolio or talk about it.

Cos it doesn't mean anything. Everything is within yourself.

How happy you are with life, your securities, your insecurities, how much you feel you need, whether you are procrastinating, what you fill your life with...

It's all about you.

And even more so... I've come to realize that the portfolio is hardly the most important thing to make someone happy. Or leaving your job.

Read about happiness is a decision here.

Some people are happy working, some people are happy working part time and get sufficient money but not a lot of money. Others are comfortable and just hang around in the job and just feeling contented but not necessarily happy.

And all of these are all ok.

So I tend to like to share all these other factors of life instead of talk about the portfolio.

And leave the portfolio and investments to other bloggers, or in the readers own hands.

*Hmm... or maybe my portfolio is too small and I don't want to share it or discuss it. Hahaha...

** This post is supposed to be posted on Monday cos I'm travelling and probably won't have time to write much. Unfortunately, I clicked post and Weebly doesn't allow me to unpost, so... Maybe Monday won't have a post, depends if I have time to write one.

<<PREVIOUS POST // NEXT POST>>

Did you like this post? If so, could you "blanjah" me 1/4 cup of my morning coffee pls.

You may also consider subscribing to receive the articles in your email, link in the column on the right.

RSS Feed

RSS Feed