Many thanks for all those who gave ideas on how I could prevent myself from forgetting to pay my credit card bills next time.

I think I'll likely set an alarm 2 times a month to remind me to check all my credit cards twice a month.

Anyway moving on...

I almost missed this...

UOB ONE ACCOUNT IS HAVING AN UPDATE FOR THEIR INTEREST RATES!!!

Imagine my shock. I went to visit my parents on Saturday and my MUM told me that there is going to be an update for UOB One account interest rates. She received an SMS about this change and I didn't!!!

I didn't get any flier, brochure, mailer... nothing... amazingly my mum is more up to date than me...

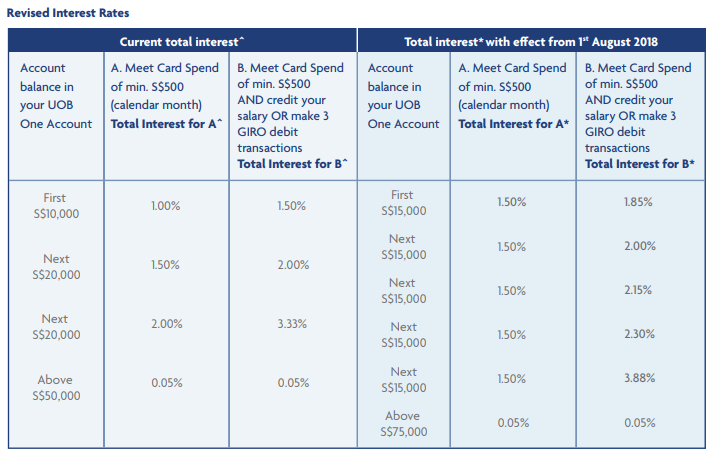

Ok anyway is the main change.

Previously (Before 1 Aug 2018), if you put in $50,000 into the UOB One account AND spend $500 on their credit card, you will get around 1.6% on the $50k. Around $800 per annum.

IF you put in $50,000 AND spend $500 on their credit card AND (credit your salary OR set up 3 GIRO txns per month), then you get 2.43% on the $50k. Around $1,215 per annum.

Updated, 1 Aug 2018 onwards, interest as usual will be paid in tiers. But now, it is up to $75,000.

So IF you put in $75,000 and spend $500 on the credit card, you will only earn 1.5% per annum, but since it is now a larger base, total interest for the year will be $1,125.

IF you put in $75,000 AND spend $500 on their credit card AND (credit your salary OR set up 3 GIRO txns per month), then you get 2.44% on the $75,000.

This is more interest AND on a larger base. Which will result in $1,830 interest per annum. Or around $152 per month for 1 account.

For 2 accounts it's $304 which is typically more than I spend on food in a normal month.

Info can all be found here in the update pdf.

I think I'll likely set an alarm 2 times a month to remind me to check all my credit cards twice a month.

Anyway moving on...

I almost missed this...

UOB ONE ACCOUNT IS HAVING AN UPDATE FOR THEIR INTEREST RATES!!!

Imagine my shock. I went to visit my parents on Saturday and my MUM told me that there is going to be an update for UOB One account interest rates. She received an SMS about this change and I didn't!!!

I didn't get any flier, brochure, mailer... nothing... amazingly my mum is more up to date than me...

Ok anyway is the main change.

Previously (Before 1 Aug 2018), if you put in $50,000 into the UOB One account AND spend $500 on their credit card, you will get around 1.6% on the $50k. Around $800 per annum.

IF you put in $50,000 AND spend $500 on their credit card AND (credit your salary OR set up 3 GIRO txns per month), then you get 2.43% on the $50k. Around $1,215 per annum.

Updated, 1 Aug 2018 onwards, interest as usual will be paid in tiers. But now, it is up to $75,000.

So IF you put in $75,000 and spend $500 on the credit card, you will only earn 1.5% per annum, but since it is now a larger base, total interest for the year will be $1,125.

IF you put in $75,000 AND spend $500 on their credit card AND (credit your salary OR set up 3 GIRO txns per month), then you get 2.44% on the $75,000.

This is more interest AND on a larger base. Which will result in $1,830 interest per annum. Or around $152 per month for 1 account.

For 2 accounts it's $304 which is typically more than I spend on food in a normal month.

Info can all be found here in the update pdf.

Ok so simply put, this is a great update. Cos it allows us to now get 2.44% interest on a larger amount of money.

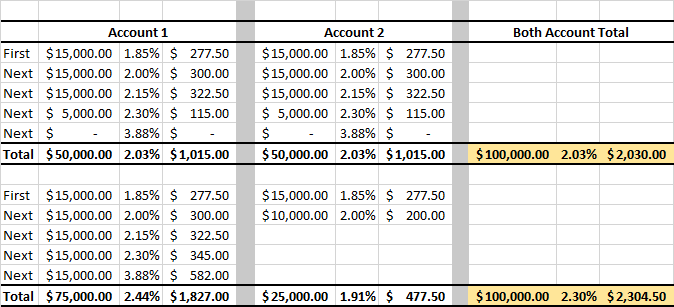

Now the problem is... not all of us has an additional $25k to top up our accounts.

If we look at someone like me. I manage 2 accounts. My wife's and my own. Where am I going to suddenly find another $50,000 to top up both our accounts.

That's going to be tough on short notice. So what should we do? I only have 4 days notice.

Well based on the calculation above, if we keep $50k in each account with the new interest rate, we would end up with 2.03% for 1 year.

IF we accumulate all the funds into $75,000 and $25,000 in the 2nd account, then we can get 2.30% interest for a year.

So based on this, we should accumulate our funds in one account to max out the $75k in one account before slowly accumulating money in the 2nd accound to build up the funds to $75k as well.

2.44% per annum is a pretty good return.

So if I look at it at a total return basis.

I have to spend $6,000 on essential spending every year.

And I will get around $1,830 in interest for this account.

I further get another $200 in credit card rebates. ($50 per quarter)

Total return I get is $2,030.

This is like getting a 34% discount on my $6,000 annual credit card spending.

Cos for me, I attribute all these returns to the spending. Cos IF I don't maintain this level of spending, then I don't get any returns or bonus interest. However, due to me maintaining this level of spending, I will get this "return" and I take it as a "discount" on all the spending which I made for the year.

Well... looks like it's time to start boosting your savings up to $75k if you don't already have it then...

Hope some of you were more updated than me.

<<PREVIOUS POST // NEXT POST>>

Did you like this post? If so, could you "blanjah" me 1/4 cup of my morning coffee pls.

You may also consider subscribing to receive the articles in your email, link in the column on the right.

RSS Feed

RSS Feed