I don't own an endowment plan...

But I think it's a pretty good product for a lot of people...

Ok ok. Before any of you start screaming about what a hypocrite I am...

Let's think about it...

Many people do not have the discipline to save regularly.

Many people do not have much insurance coverage.

A lot of people do not invest or they get FD returns of around 1%.

I'm talking about the large percentage of Singaporeans here...

Now knowing this... wouldn't an endowment plan be great for their financial planning purposes?

Let's say a young person just coming out to work.

25 years old, he could get a low premium endowment plan each month. Maybe $100 per contribution per month and the term of the plan should be until he is 65 years old.

It's a simple forced savings with insurance coverage as well.

He may not be financially inclined and may not do much investments or may be risk adverse and avoid investments his whole life. There are many people who just do not like doing investments cos they cannot sleep well at night due to the swings in the market.

As he grows older, he earns more, he can buy another endowment plan at maybe 30 years old, once again term of the plan until he is 65 years old. He can contribute whatever he feels comfortable to contribute.

He can continue to stack up his contribution and buy new policies until around 55 years old. Of which the returns drop cos there's not enough time for compounding.

By the time he reaches 65, he would have a nice lump sum for him to slowly retire, or he could switch to buying Singapore Savings Bonds, with the lump sum, if SSBs are still around at that time.

If we think about it from a very normal perspective, I think endowment plans are a pretty good product for many people. A long term endowment plan gives returns of something like 3% annually if allowed to compound long enough. It's a form of forced savings and insurance. Many people don't save diligently with monthly discipline. It also locks up their money so they won't have the inclination to spend it all.

Many people might not have a lump sum of $10,000 (<-incorrect) to buy a SSB straight out and there's no insurance coverage as well. And many Singaporeans ARE under insured...

Edited: SSB minimum purchase is only $500 as pointed out by InvestWizard.

Nonetheless, SSB requires an individual to go down to proactively purchase it every few months, an endowment can be simply set with GIRO payments to auto deduct every month. For a regular person, this is a much better arrangement.

Yes it's likely that an individual would do better if he buys term insurance and invests the rest, but how many people are like that? If I look at the general population, I would think 70% of people should be buying an endowment plan. It would do them good in the long run.

Not all endowment plans are made well. Personally, I would choose a low cost endowment plan. I think Prudential has one of the highest fees with the lowest capital guaranteed. I think Tokio Marine has the highest capital guaranteed with low fees, but it's less well known. I think maybe Great Eastern would be a good balance. Cos it's backed by OCBC and the fees are relatively low so there's a greater confidence that they will still be around 30 years from now.

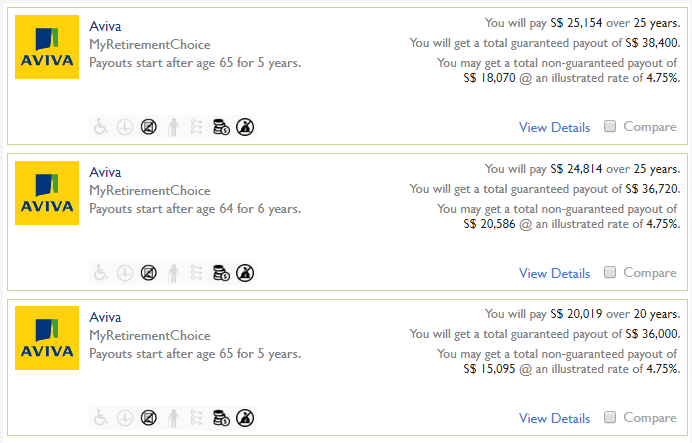

Edit : Did some estimation on http://www.comparefirst.sg

Aviva seems to have a better guaranteed payout which is better than Great Eastern or Prudential.

I estimated based on 35 age next birthday, male, non smoker, for 25 years.

But I think it's a pretty good product for a lot of people...

Ok ok. Before any of you start screaming about what a hypocrite I am...

Let's think about it...

Many people do not have the discipline to save regularly.

Many people do not have much insurance coverage.

A lot of people do not invest or they get FD returns of around 1%.

I'm talking about the large percentage of Singaporeans here...

Now knowing this... wouldn't an endowment plan be great for their financial planning purposes?

Let's say a young person just coming out to work.

25 years old, he could get a low premium endowment plan each month. Maybe $100 per contribution per month and the term of the plan should be until he is 65 years old.

It's a simple forced savings with insurance coverage as well.

He may not be financially inclined and may not do much investments or may be risk adverse and avoid investments his whole life. There are many people who just do not like doing investments cos they cannot sleep well at night due to the swings in the market.

As he grows older, he earns more, he can buy another endowment plan at maybe 30 years old, once again term of the plan until he is 65 years old. He can contribute whatever he feels comfortable to contribute.

He can continue to stack up his contribution and buy new policies until around 55 years old. Of which the returns drop cos there's not enough time for compounding.

By the time he reaches 65, he would have a nice lump sum for him to slowly retire, or he could switch to buying Singapore Savings Bonds, with the lump sum, if SSBs are still around at that time.

If we think about it from a very normal perspective, I think endowment plans are a pretty good product for many people. A long term endowment plan gives returns of something like 3% annually if allowed to compound long enough. It's a form of forced savings and insurance. Many people don't save diligently with monthly discipline. It also locks up their money so they won't have the inclination to spend it all.

Many people might not have a lump sum of $10,000 (<-incorrect) to buy a SSB straight out and there's no insurance coverage as well. And many Singaporeans ARE under insured...

Edited: SSB minimum purchase is only $500 as pointed out by InvestWizard.

Nonetheless, SSB requires an individual to go down to proactively purchase it every few months, an endowment can be simply set with GIRO payments to auto deduct every month. For a regular person, this is a much better arrangement.

Yes it's likely that an individual would do better if he buys term insurance and invests the rest, but how many people are like that? If I look at the general population, I would think 70% of people should be buying an endowment plan. It would do them good in the long run.

Not all endowment plans are made well. Personally, I would choose a low cost endowment plan. I think Prudential has one of the highest fees with the lowest capital guaranteed. I think Tokio Marine has the highest capital guaranteed with low fees, but it's less well known. I think maybe Great Eastern would be a good balance. Cos it's backed by OCBC and the fees are relatively low so there's a greater confidence that they will still be around 30 years from now.

Edit : Did some estimation on http://www.comparefirst.sg

Aviva seems to have a better guaranteed payout which is better than Great Eastern or Prudential.

I estimated based on 35 age next birthday, male, non smoker, for 25 years.

So if you think about it this way, isn't an endowment plan a pretty good product?

I'm sure you know of at least 1 person who would actually benefit from buying an endowment plan.

Cos the truth is...

Many people do not have the discipline to save regularly,

Many people do not invest their excess funds at better than FD rates,

Some people do not sleep well having their funds exposed to market conditions,

Many people are under-insured,

not to mention a lot of people would spend whatever money they have if they saved up a lump sum, so locking up the money is also very good for them.

Once again, please note this post is my personal opinion, an endowment plan may or may not be suitable for your financial planning purposes, please seek professional advice if you are not sure of what to do from a reputable financial adviser. I'm not endorsing any of the companies which I have mentioned in the post. Blah blah blah, you get the picture.

It's pretty tiring typing out these disclaimers... blah blah blah... please don't blame me if you screw up in the future, please do your own research.

A financial plan is a holistic plan not just a patch work of products that you buy a little here and buy a little there. So please do a needs based analysis which a qualified financial adviser will ask you to do. But likely he/she won't do it well, and you will need sign it off regardless of how poorly it was done so that you can cover the a$$ of the financial institution selling the product.

<<PREVIOUS POST // NEXT POST>>

Did you like this post? If so, could you "blanjah" me 1/4 cup of my morning coffee pls.

Many thanks for continuing to come to this blog to read my posts.

RSS Feed

RSS Feed