So when I got my HDB couple of years back, we took the POSB HDB Loan instead of the HDB Loan.

The interest rate for this POSB Loan is some mix of short term and long term fixed deposits + a fixed percentage. The best part of this loan is that it is maxed at 2.5% for 8 years. For the past 3+ years, the interest rate has been higher than most floating rate loans but lower than 2.5%. It has been slowly increasing the past few years. Recently, I just received a letter from DBS/POSB to tell me that the interest rate is now at 2.5%.

Also, there is no penalty for prepayment or partial prepayment of the loan.

Now, of course I have already been paying a lower interest rate than many folks who bought their HDB using the HDB Loan, cos that's 2.6% straight out. Which is 0.1% more than CPF interest rate.

For years, we could have paid off our home loan using our CPF funds. However, since CPF rate was higher than our loan rate, we didn't bother to.

Now that our mortgage interest is equal to CPF rate, what should we do?

Ok by right, all money is the same. So money in CPF vs money in the bank is the same.

CPF is currently giving 2.5%

Bank is giving a little less than 2.5%, if you are able to capitalize on the UOB One account, or DBS Multiplier account or OCBC 360 account.

If you are invested in the stock market, then dividends could be more or less, capital gains could be more or less. This is the same for bonds.

IF you are NOT invested in anything and the returns on your excess funds is the base interest rate from bank deposits, which is under 1%... Then you should use cash to pay up the POSB HDB Loan...

So that's what we did, or have been doing. For the past 1 year or so, as interest rates were rising, we have been using any new liquidity to settle our loan, so maybe we have some extra returns from some of our investments, or if I sell down some of our investments, or if she has excess from her salary, we use it to pay down the housing loan.

Now, of course, different people have different uses for their money or how they want to invest and get returns for their money. 2.5% is considered a low interest rate. Many people might not want to pay down the loan and instead use the extra money to invest in blue chips and probably get a better rate of return.

This is absolutely fine and probably a good idea.

For us, we have decided to take a more prudent approach. We still have some funds set aside making around 2% return, waiting for a good opportunity in the stock market. Besides this, we decided that all excess funds should go to paying off the housing loan.

The thing is... even though I know that there is a high chance that the stock market will provide more than 2.5% return in the long run, I cannot 100% guarantee it. So we have set aside a sum for investments, and any excess to be used to pay off our housing loan.

This has in part been due to my past experience when investing. During the banking crisis in 2007, I invested too early and the market had not dropped enough yet. I was sitting on around 40% losses for months/years. Even though I recovered those losses and more, the lesson I took back was that I need to be able to wait out any losses and that my AUM could drop very quickly due to bad market conditions.

The thing is... currently, we are able to pay off our loan at any time. However, I do not want to do that yet, cos these funds are set aside to capitalize on any market opportunities.

We do eventually want to pay off our loan. We don't want to end up from a position where we can pay off my loan, then make some investment at a wrong time and end up in a position where we are unable to fully settle our loan.

So we decided to set aside a certain sum of funds which we feel is reasonable for investment, and any excess we use to quickly pay off the housing loan.

There are a few ways to approach retirement planning.

I agree that 2.5% is a low rate of interest and most people would not prepay their mortgage and instead use the funds to further invest.

In a way, this is aggressive, cos they are taking a loan to invest.

They take a loan on the house, if they have excess funds they don't prepay the loan but instead use the money to invest, this actually means they are taking a loan to invest.

For us, we are in a more defensive aggressive mode.

Cos we have more or less stabilized our lives. The house can be fully paid up, but if we do that, then the amount for investment will drop by quite a large sum. We feel that this amount set aside is large enough but not too large. We estimate that it is sufficient to prepare us for our future financial needs.

And now we want to fully pay off our housing loan to get that off our minds.

Maybe I can explain better in the below chart.

The interest rate for this POSB Loan is some mix of short term and long term fixed deposits + a fixed percentage. The best part of this loan is that it is maxed at 2.5% for 8 years. For the past 3+ years, the interest rate has been higher than most floating rate loans but lower than 2.5%. It has been slowly increasing the past few years. Recently, I just received a letter from DBS/POSB to tell me that the interest rate is now at 2.5%.

Also, there is no penalty for prepayment or partial prepayment of the loan.

Now, of course I have already been paying a lower interest rate than many folks who bought their HDB using the HDB Loan, cos that's 2.6% straight out. Which is 0.1% more than CPF interest rate.

For years, we could have paid off our home loan using our CPF funds. However, since CPF rate was higher than our loan rate, we didn't bother to.

Now that our mortgage interest is equal to CPF rate, what should we do?

Ok by right, all money is the same. So money in CPF vs money in the bank is the same.

CPF is currently giving 2.5%

Bank is giving a little less than 2.5%, if you are able to capitalize on the UOB One account, or DBS Multiplier account or OCBC 360 account.

If you are invested in the stock market, then dividends could be more or less, capital gains could be more or less. This is the same for bonds.

IF you are NOT invested in anything and the returns on your excess funds is the base interest rate from bank deposits, which is under 1%... Then you should use cash to pay up the POSB HDB Loan...

So that's what we did, or have been doing. For the past 1 year or so, as interest rates were rising, we have been using any new liquidity to settle our loan, so maybe we have some extra returns from some of our investments, or if I sell down some of our investments, or if she has excess from her salary, we use it to pay down the housing loan.

Now, of course, different people have different uses for their money or how they want to invest and get returns for their money. 2.5% is considered a low interest rate. Many people might not want to pay down the loan and instead use the extra money to invest in blue chips and probably get a better rate of return.

This is absolutely fine and probably a good idea.

For us, we have decided to take a more prudent approach. We still have some funds set aside making around 2% return, waiting for a good opportunity in the stock market. Besides this, we decided that all excess funds should go to paying off the housing loan.

The thing is... even though I know that there is a high chance that the stock market will provide more than 2.5% return in the long run, I cannot 100% guarantee it. So we have set aside a sum for investments, and any excess to be used to pay off our housing loan.

This has in part been due to my past experience when investing. During the banking crisis in 2007, I invested too early and the market had not dropped enough yet. I was sitting on around 40% losses for months/years. Even though I recovered those losses and more, the lesson I took back was that I need to be able to wait out any losses and that my AUM could drop very quickly due to bad market conditions.

The thing is... currently, we are able to pay off our loan at any time. However, I do not want to do that yet, cos these funds are set aside to capitalize on any market opportunities.

We do eventually want to pay off our loan. We don't want to end up from a position where we can pay off my loan, then make some investment at a wrong time and end up in a position where we are unable to fully settle our loan.

So we decided to set aside a certain sum of funds which we feel is reasonable for investment, and any excess we use to quickly pay off the housing loan.

There are a few ways to approach retirement planning.

I agree that 2.5% is a low rate of interest and most people would not prepay their mortgage and instead use the funds to further invest.

In a way, this is aggressive, cos they are taking a loan to invest.

They take a loan on the house, if they have excess funds they don't prepay the loan but instead use the money to invest, this actually means they are taking a loan to invest.

For us, we are in a more defensive aggressive mode.

Cos we have more or less stabilized our lives. The house can be fully paid up, but if we do that, then the amount for investment will drop by quite a large sum. We feel that this amount set aside is large enough but not too large. We estimate that it is sufficient to prepare us for our future financial needs.

And now we want to fully pay off our housing loan to get that off our minds.

Maybe I can explain better in the below chart.

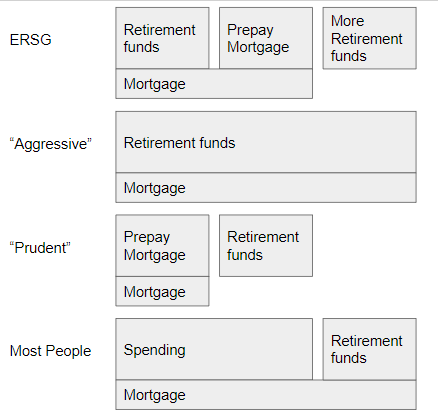

For us, we have been paying our mortgage slowly throughout the years but also heavily planning for retirement. We have reached a certain AUM which we feel is fairly good, so we think its better for us to clear off our loan before accumulating more retirement funds.

There will be many other financially savvy folks who would continue to hold the low interest rate loan and pay their mortgage slowly throughout the years whilst accumulating their retirement funds.

I find this to be absolutely reasonable thinking. I have friends like this.

Just that for me, we find the above works better for us.

Then there will also be folks who focus on prepaying their mortgage first before planning for their retirement funds. I know people like this.

Then there will be what most people do...

They pay off their mortgage throughout the years using their CPF, then they don't think about retirement and live it up.

Then when they reach 50-60 years old, they suddenly realize they need to retire eventually, then they start planning and stressing about it.

I also know people like this...

Well, anyway, that's what we're planning to do with our loan. Our interest rate started at 1.88% and it's now 2.5%, and hopefully, soon it will be down to ZERO...

**EDIT**

My wife opened the bank letter. I didn't realize it was actually 2.455% and she rounded it up when she told me that the interest had increased to 2.5%.

<<PREVIOUS POST // NEXT POST>>

Did you like this post? If so, could you "blanjah" me 1/4 cup of my morning coffee pls.

You may also consider subscribing to receive the articles in your email, link in the column on the right.

There will be many other financially savvy folks who would continue to hold the low interest rate loan and pay their mortgage slowly throughout the years whilst accumulating their retirement funds.

I find this to be absolutely reasonable thinking. I have friends like this.

Just that for me, we find the above works better for us.

Then there will also be folks who focus on prepaying their mortgage first before planning for their retirement funds. I know people like this.

Then there will be what most people do...

They pay off their mortgage throughout the years using their CPF, then they don't think about retirement and live it up.

Then when they reach 50-60 years old, they suddenly realize they need to retire eventually, then they start planning and stressing about it.

I also know people like this...

Well, anyway, that's what we're planning to do with our loan. Our interest rate started at 1.88% and it's now 2.5%, and hopefully, soon it will be down to ZERO...

**EDIT**

My wife opened the bank letter. I didn't realize it was actually 2.455% and she rounded it up when she told me that the interest had increased to 2.5%.

<<PREVIOUS POST // NEXT POST>>

Did you like this post? If so, could you "blanjah" me 1/4 cup of my morning coffee pls.

You may also consider subscribing to receive the articles in your email, link in the column on the right.

RSS Feed

RSS Feed